| Blog

| Blog

| Blog

| Blog

23 October 2020

When it comes to buying your first home, it can often feel like you’re going back to school. From learning a new mortgage language and trying to understand your LTV from your AIP (scroll down for our Mortgage Lingo Cheat Sheet), to doing the maths when trying to understand the various mortgage rates available to you, do you go with 2% or 3%? The good thing is you may actually have some spending money this time round, yes that’s right with our mortgage cashback offer you can get 2% cashback at drawdown on your mortgage with permanent tsb to help you get started! But what does it all really mean and how can you make sure you’re getting the best mortgage for you? We’re here to support you at every stage of your journey, so to help you through your mortgage research, we’ve outlined what you need to know from mortgage rates, mortgage jargon, cashback mortgage offers and everything in between.

It can often be hard to navigate the various mortgage rates on offer so we’ve broken down the different options below to help you figure out which rate type is right for you and you needs. We’ve actually lowered our mortgage rates meaning you’ll have lower monthly repayments and see real savings on your mortgage with our lowest rates ever. That said, should you need any help figuring out the best rate for you and your situation, it’s a good idea to come in and talk to our mortgage team who can take you through the different mortgage interest rate options, so if you’re looking for that personal steer why not book an appointment today.

Whether you choose a Fixed or a Variable rate mortgage will depend on your financial circumstances and your attitude to risk. With a fixed rate mortgage, your interest rate and monthly repayments are fixed for a set time so your repayments will stay the same and you’ll know what you will be paying each month. This can give you a nice sense of security while you settle into your new home.

Although you’ll have peace of mind with a fixed rate knowing your repayments will not rise during the fixed rate period, your repayment will not fall either meaning you could miss out on lower interest rates and lower repayments so a fixed rate may cost more over the long run. It’s also good to keep in mind that if you did want to pay off a fixed rate loan early, charges may apply. A lot of people start out with a fixed rate and then move onto a variable rate when they’re settled into their mortgage but it’s good to chat through the different options available to you with a mortgage consultant to make sure you’re happy with the rate you’re choosing.

Variable rates offer the most flexibility when it comes to mortgage rates. They allow you to increase your repayments, use a lump sum to pay off all or part of your mortgage or re-mortgage without having to pay any fixed rate breakage fees. While this can be appealing, remember that variable rates can rise and fall so your mortgage repayments can increase or decrease during the term of your loan which is something to keep in mind if you’re just starting out on your mortgage journey.

If you’ve already started out on your home buying journey and have a house buying budget in mind and a deposit goal then check out our Mortgage Rate Selector Tool which can help you by drilling down to the mortgage rate options that specifically match your criteria. For example you can be eligible for different mortgage rate options depending on the value of your mortgage or the size of your deposit so this tool will clearly outline all your options and help you figure out the best mortgage rate for you.

As you start out on your home buying journey, you’ll come across quite a few new terms and acronyms which can almost feel like a new language. If you’re struggling to make sense of the mortgage lingo, there’s no need to break out the thesaurus as we’re here to help you get to grips with it all. We’ll let you know what we mean when we talk about stuff like equity and AIP (Approval in Principle). Our Mortgage Jargon Buster will help you understand everything you need to know when it comes to mortgages.

When doing your research and getting mortgage ready, you’ll need to be sure you take some time to understand all the extra costs you’ll need to take into account. You don’t want these delaying you when you’re in those final stages and ready to drawdown your mortgage on your dream home. We’ve outlined some of these costs below so you can get up to speed and factor them into your savings early on.

Stamp duty of 1% applies to properties up to €1m, and it’s 2% on anything above €1m. To take a real world example, on a property going for €350,000, you’d need to factor in saving €3,500 to cover this cost.

Many solicitors charge a percentage amount (normally around 1% of the mortgage) to look after the legal aspects of buying a house. Get your solicitor on a mate’s recommendation – and be choosy. You’ll need them as your failsafe sidekick when it comes to contract time.

Before committing to the purchase, it’s a good idea to have a professional carry out a structural survey of the property. A seller is under no obligation to tell you about any defects. Your bank will need a valuation for the mortgage application, but a survey will be more in-depth and tell you everything you need to know about every nook and cranny of the gaff. That’s need to know info!

You will need to take out both mortgage protection insurance (a type of life insurance) and in some cases building insurance when getting a mortgage to buy your home, we can take you through the requirements at your mortgage appointment. This is for your own protection to ensure you’re fully covered should anything happen, so don’t forget to take these into consideration when saving too.

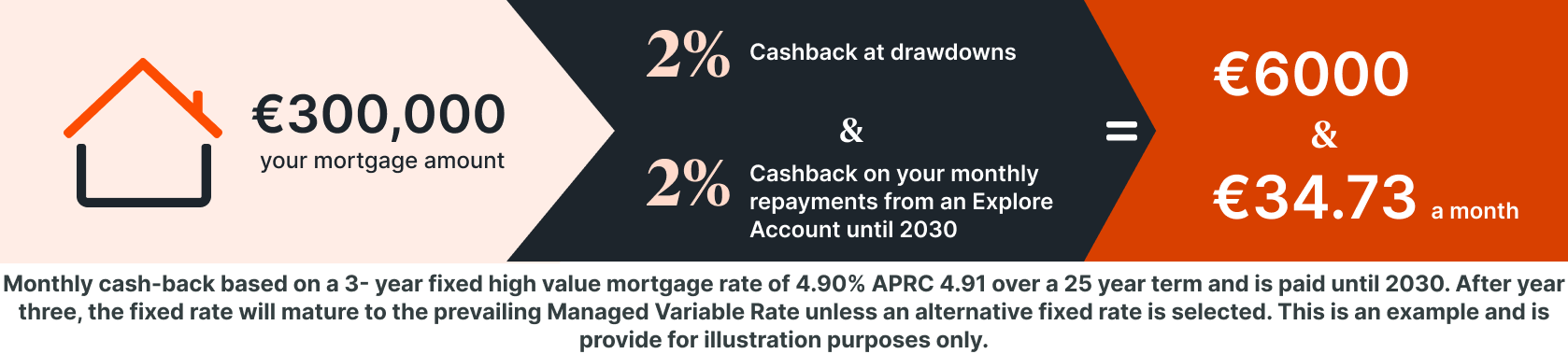

Finding your dream house is only the first step in making it your home. To help you get started putting your own stamp on the place, we offer cashback at drawdown as part of our mortgage offer, so you’ll get 2% of your mortgage value back in cash to help you make the place your own. For example, if you take out a €300,000 mortgage you’ll get €6,000 back as cash. To receive this 2% cashback you must have received your full Letter of Approval on or before 31 December 2021. This 2% cashback offer is available to both fixed and variable rate customers, so you can choose which suits you best. You also don’t need to have a permanent tsb current account to avail of this. When you drawdown your mortgage, the cashback is paid into your mortgage paying account within 40 working days so you’ll have some time to figure out what’s best to spend it on and what you really need. So whether you’ve already picked out your dream couch or have your eye on that flat screen TV, you’ll have your mortgage cashback in your back pocket to get you started.

Wherever you are on your home buying journey we’re here to support you along the way so book an appointment to start your journey home with us today or find out more over on our Mortgage Section on our website.

Offer available to new applicants who receive full letter of approval within the qualifying period. Excludes tracker, buy-to-let, negative equity and applicants refinancing an existing permanent tsb mortgage. 2% cashback at drawdown is paid into the customer’s mortgage paying account within 40 working days of mortgage drawdown. The qualifying period (11 January 2016 until 30 June 2022) may be extended as permanent tsb decides.Rates available to new and existing home mortgage customers only. Product eligibility criteria applies. Lending criteria, terms and conditions apply. Security and Insurance required. permanent tsb p.l.c is regulated by the Central Bank of Ireland.

The content of this blog does not constitute advice and is for general information purposes only. Readers should always seek professional advice before relying on anything stated in the blog. Some of the links above bring you to external websites. Your use of an external website is subject to the terms of that site.

Open24

Open24