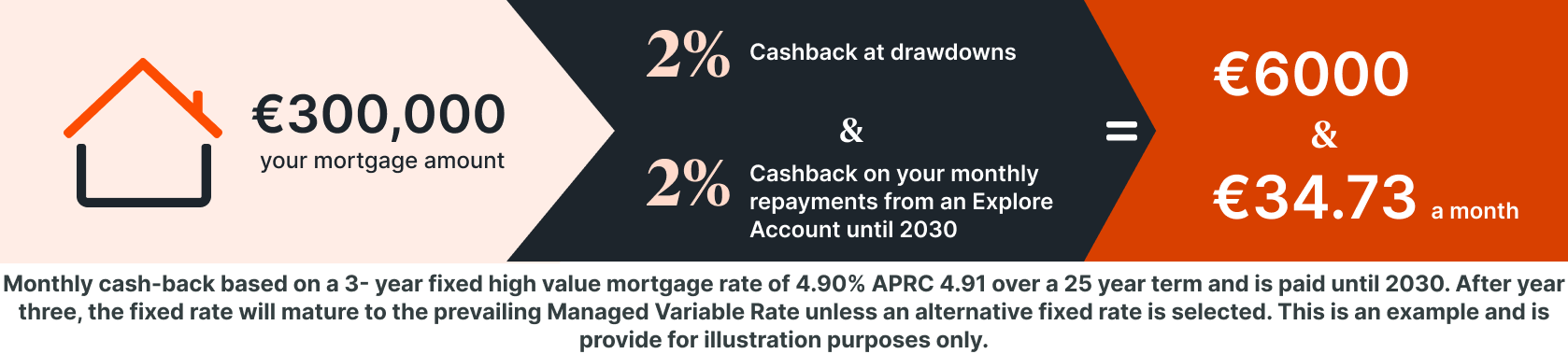

We can help get you moving. And 2% cashback at drawdown and 2% cashback on your monthly repayments from an Explore Account until 2030 can help you move in.

Whatever your mortgage needs, we have a range of competitive mortgage rates so you can choose the rate that’s right for you and we offer flexible repayment options which could make your mortgage easier to manage.

Take some time to review all the information below to ensure you have all the necessary details before starting your application with us.

With our Online Mortgage Portal you can now start your application, track your progress and talk to us when you need us. If you start your application online, you will still have the option to meet a Mortgage Consultant in person. Or you can still book an appointment in branch or in a place that suits you.

Apply Online Book an appointment Call 0818 50 24 24

Note: The fixed rates will mature to the prevailing LTV Managed Variable Rate. The applicable maturity rate will be based on the loan to value at account opening.

Excludes 4 Year Fixed Home Loan New Business Rates, tracker, buy-to-let, negative equity and applicants refinancing an existing PTSB mortgage

The above information is valid as 17 January 2024

2% cashback at drawdown will be paid on the amount of the mortgage advanced. 2% cashback at drawdown is paid into the customer’s mortgage paying account (which does not need to be a PTSB account) within 40 working days of mortgage drawdown. The qualifying period (11 January 2016 until 31 March 2025) may be extended as PTSB decides. 2% cashback at drawdown excludes 4 Year Fixed Home Loan New Business Rates, tracker, buy-to-let, negative equity and applicants refinancing an existing PTSB mortgage.

2% cashback monthly will be paid until 31/12/2030. Your monthly mortgage repayment must be made from a PTSB Explore Account and meet qualifying criteria. Only mortgage payments made by Direct Debit from an Explore Account will get the 2% cashback monthly. The Explore Account carries a €8 monthly fee for maintaining the account. Any items that are returned unpaid (including Direct Debits and Standing Orders) will incur the appropriate unpaid item charge and other charges may apply. eStatements only. If any changes to the billed monthly mortgage repayment are made they must be agreed by both you and PTSB to be eligible for the cashback monthly offer.

If either the Explore Account or the Mortgage is terminated for any reason then the monthly cashback will cease. PTSB retains the right to close the Explore Account as per the General Terms & Conditions. Offer applies to home loans only i.e. excludes buy-to-lets. It should be noted that any change in use of the property from personal use to letting could have tax implications for you.

See here for more information about the unique benefits of the Explore Account from PTSB.

Information correct as of 29 January 2024 but is subject to change.

72 hours starts once your application is completed and submitted for credit assessment during business hours. Excludes weekends. If any documentation is missing or additional information is required to reach a credit decision, we will notify you which may impact the decision time.

Lending criteria, terms and conditions apply. Mortgage approval is subject to assessment of suitability and affordability. Applicants must be aged 18 or over. Security and home and life insurance are required. Rates available to new and existing home mortgage customers only. Maximum loan to value is 90%.

For First Time and Second Time Buyers a maximum Loan to Value (LTV) of 90% will apply to a property’s purchase price. The maximum LTV for customers who hold their current mortgage with another bank but wish to switch their mortgage to PTSB while also releasing equity is 85%. Maximum loan amount will typically not exceed 4 times an individual’s gross income for First time Buyers & 3.5 times an individual’s gross income for Second time Buyers.

The monthly repayment on a 20 year mortgage with Loan to Value (LTV) greater than 80% with variable borrowing rate of 4.70% on mortgage of €100,000 is €643.50 for 240 months. Total amount repayable is €154,799.06. If interest rates increase by 1% an additional €55.73 would be payable per month. For this example, Annual Percentage Rate of Charge (APRC) of 4.84% applies and consists of variable borrowing rate of 4.70%, valuation fee of €150, Property Registration Authority (PRA) fee of €175, and security vacate fee of €35. Please note – this APRC does not factor in the €8 monthly fee for maintaining the Explore Account.

Certain flexible mortgage repayment options can only be used one at a time and may result in additional interest costs over the term of the loan. Full details available on here on our website, in branch or over the phone.

Changing the repayment date may result in additional interest charged to take account of daily interest accumulated between the previous and new repayment dates. Full details available here on our website, in branch or over the phone.

'Skip a maximum of 2 monthly mortgage repayments each year. The monthly repayments due over the remaining 10 or 11 months of the year will be increased to take account of the amount(s) not paid. To qualify loan must be paid by Direct Debit or Standing Order from a PTSB account. Full details available here on our website, in branch or over the phone.

Warning: You may have to pay charges if you pay off a fixed-rate loan early.

Warning: The cost of your monthly repayments may increase.

Warning: If you do not keep up your repayments you may lose your home.

Warning: If you do not meet the repayments on your loan, your account will go into arrears. This may affect your credit rating, which may limit your ability to access credit, a hire-purchase agreement, a consumer-hire agreement or a BNPL agreement in the future.

You can now start, and track the progress of your mortgage journey online with our new mortgage portal. If you start your application online, you will still have the option to meet a Mortgage Consultant in person.

Or you can still book an appointment in branch or in a place that suits you.

Apply online Book an appointment Call 0818 50 24 24